When it is comes to personal finance, APR (Annual Percentage Rate) & APY (Annual Percentage Yield) are two that confuse people. both involve interest, both are expressed as a percentage, and both directly impact how much you’ll earn on savings or pay on loans. However, the way they work—and the way financial institutions present them—are very different.

What Is APR (Annual Percentage Rate)?

The Annual Percentage Rate (APR) is the borrowing money, expressed yearly percentage. Unlike a simple interest rate, APR often includes fees, points, and other loan-related charges that make it a more accurate reflection of what you’ll pay.

For example, if you take out a loan for $10,000 at a 6% interest rate but also pay a $500 origination fee, your APR will be higher than 6% because it incorporates that fee into the total cost of borrowing.

Key Features of APR:

- Represents borrowing costs over one year.

- Includes fees and charges (not just interest).

- Does not account for compound interest.

- Required by law (via the Truth in Lending Act) to be disclosed to borrowers.

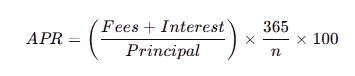

Formula for APR:

Where:

- Fees = upfront charges and costs

- Interest = total interest paid

- Principal = amount borrowed

- n = loan term in days

This calculation gives borrowers a standardized way to compare loan offers.

What Is APY (Annual Percentage Yield)?

The Annual Percentage Yield (APY) measures how much interest you’ll earn on savings or deposits over a year, factoring in compound interest. Compounding means you’re not only earning interest on your initial deposit but also on the interest that accumulates over time.

For example, if you deposit $5,000 in savings account at 5% interest, your APY will be slightly higher than 5% if the interest is compounded monthly. That’s because each month, the new balance grows a little larger as the previous month’s interest is added to it.

Key Features of APY:

- Represents earnings from savings or investments.

- Includes the effect of compound interest.

- The more frequently interest compounds, the higher the APY.

- Required by law to be disclosed by banks for savings accounts and CDs.

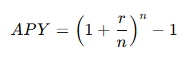

Formula for APY:

Where:

- r = interest rate

- n = number of compounding periods per year

APR vs. APY: The Core Difference

The main difference between APR and APY lies in compounding:

- APR: Shows the annual cost of borrowing, including fees but not compounding.

- APY: Shows the annual return on savings, including the effects of compounding.

To put it simply:

- APR benefits lenders (shows how much you’ll owe).

- APY benefits savers (shows how much you’ll earn).

Example: Loan vs. Savings Account

Let’s compare a loan and a savings product to illustrate the difference:

- Loan: You borrow $5,000 at a 5% APR, paid back over one year. You’ll end up paying $136.45 in interest.

- Savings: You deposit $5,000 into a 12-month CD at a 5% APY (compounded monthly). At the end of year, you will earn $255.81 in interest.

Even though both are “5%,” the impact is different because of compounding.

The Borrower’s Perspective: Why APR Matters

If you are borrowing money through an auto loan, a mortgage, a student loan, or a credit card.

Must watch for the APR number.

- A lower APR means less money paid over time.

- Lenders must disclose APR to help borrowers compare loan products.

- Credit cards typically advertise a monthly interest rate, but federal law requires them to also provide the APR.

For example, if a bank offers you a mortgage with a 5% APR, but another offers 5% APR with additional upfront fees, the actual cost of borrowing will be higher with the second lender.

The Saver’s Perspective: Why APY Matters

On the flip side, if you’re saving money, APY tells you how much your deposit will grow.

- Higher APY = more earnings.

- Frequent compounding (daily > monthly > annually) increases your APY.

- Always compare APYs when looking for high-yield savings accounts or CDs.

For example, a savings account offering 4.90% APY compounded daily will earn you more than one offering 5.00% APY compounded annually.

How Compounding Frequency Changes the Outcome

Compounding is the secret weapon of APY.

Here’s how a quoted 5% APR loan looks depending on compounding:

| Quoted APR | Semi-Annual Compounding | Quarterly | Monthly |

| 5% | 5.06% | 5.09% | 5.11% |

| 7% | 7.12% | 7.19% | 7.23% |

| 9% | 9.20% | 9.30% | 9.38% |

This small difference becomes massive over decades—especially in long-term mortgages or retirement savings.

APR vs. Interest Rate: Are They the Same?

- Interest rate = the cost of borrowing (or earning) before fees and compounding.

- APR = interest rate + fees and charges.

This is why a loan with a “low interest rate” may still have a high APR if it includes fees, points, or hidden costs.

What Is a Good APR?

A “good” APR depends on the type of loan and your creditworthiness. Generally:

- Credit cards: 15–25% APR (lower is better).

- Auto loans: 5–8% APR (varies by credit score).

- Mortgages: 6–7% APR (as of 2025 averages).

- Personal loans: 8–12% APR for borrowers with good credit.

Tip: Always compare the APR of similar loan products (e.g., compare mortgage APRs with other mortgage APRs, not with credit cards).

Which Is Better, APR or APY?

Neither is “better”—they serve different purposes:

- If you’re borrowing, focus on APR to minimize costs.

- If you’re saving or investing, focus on APY to maximize returns.

Financial institutions highlight the one that makes them look better:

- Banks promote APY for savings accounts.

- Lenders promote APR for loans.

Common Misconceptions About APR and APY

- “APR and APY are the same thing.”

→ False. APR doesn’t include compounding; APY does. - “A lower interest rate always means a better deal.”

→ Not always. Look at the APR for the real cost. - “A savings account with 5% interest rate is the same as 5% APY.”

→ Not true if compounding happens more than once a year.

Final Thoughts: Making Smarter Money Choices

Both APR and APY play a critical role in your financial life. APR affects how much you’ll pay when you borrow, while APY affects how much you’ll earn when you save.

The difference might look small on paper, but over time, these percentages can mean thousands of dollars gained or lost. That’s why it’s crucial to:

- Always compare APRs when shopping for loans.

- Always compare APYs when choosing savings products.

- Pay attention to compounding frequency, as it magnifies the impact of both.

In short, understanding APR vs. APY gives you the knowledge to borrow smarter and save wiser—putting more money in your pocket and keeping less in the hands of banks.