When you park your cash in a bank, not all deposit accounts are the same, two common types are demand deposits and term deposits, each built for different financial needs, one for flexibility, the other for stronger, but locked-in, returns.

What Is a Demand Deposit?

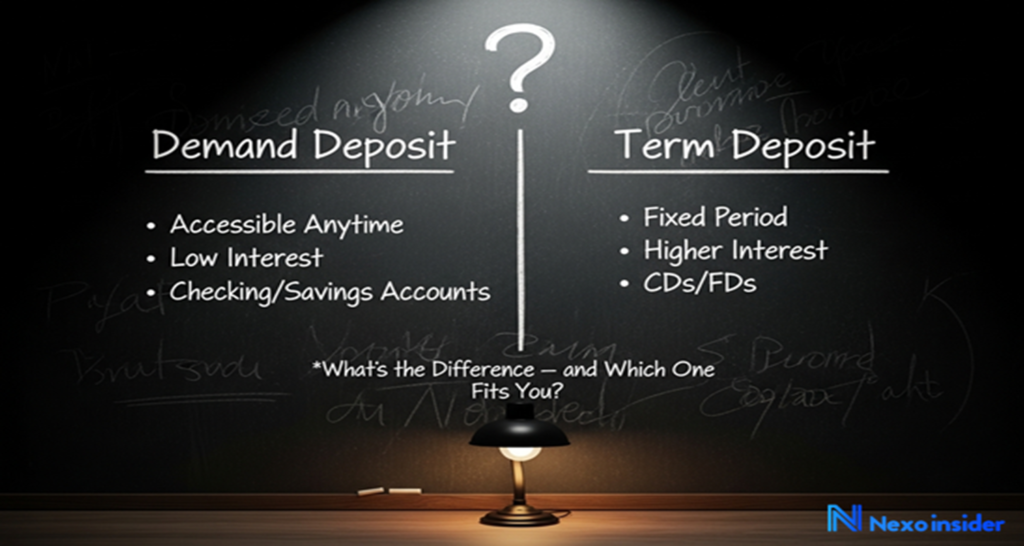

A demand deposit is a bank deposit you can access any time, on demand. There’s no waiting period, no lock-in, you can withdraw or transfer funds the moment you want. It’s the everyday “go-to” account for most of us.

Here’s how demand deposits stand out:

- Instant access — You can withdraw money via ATM, online transfer, checks, or debit card without prior notice or penalty.

- No fixed term — The funds stay available as long as the account remains open.

- Liquidity & flexibility — Ideal for daily expenses, bills, short-term cash flow, or situations where you might need quick access to funds.

- Lower interest (or none) — Because you can access money freely, banks pay little return on demand deposits compared to locked-in deposits.

Typical demand deposit accounts include checking/current accounts, and some savings or money-market–type accounts depending on bank rules.

In short: demand deposits are your liquidity backbone — handy for regular expenses, unpredictable needs, or as a buffer account.

What Is a Term Deposit?

In contrast, a term deposit (also called a time deposit) sets your money aside for a fixed time period — anywhere from a few months to several years — in exchange for a better interest rate.

Here are the hallmarks of term deposits:

- Fixed duration — When you open the deposit, you choose a maturity date. Until then, the funds stay locked.

- Higher interest rates — Because banks know the money is locked in, they reward you with better yields than typical demand deposits.

- Withdrawal restrictions — If you access the funds before maturity, you’ll likely face penalties or lose the earned interest.

- Predictable returns — Especially useful when you want to grow savings securely over time, without market risk.

Common examples include certificates of deposit (CDs) or fixed-term savings/deposit accounts offered by banks.

In short: term deposits are great for money you don’t need immediately — think long-term savings, emergency funds you won’t touch soon, or planned future expenses.

Demand Deposit vs Term Deposit: Side-by-Side Comparison

| Feature / Attribute | Demand Deposit | Term Deposit |

| Access to funds | Immediate; withdraw anytime without penalty | Locked until maturity; early withdrawal may cause penalty |

| Term / Maturity | None (open-ended) | Fixed duration decided upfront (months to years) |

| Interest rate / Return | Low or negligible (priority is liquidity) | Higher — reward for locking funds in for a term |

| Liquidity / Flexibility | High — great for everyday use, payments, cash flow | Low — best when money is not needed immediately |

| Best use case | Daily expenses, emergency fund, flexible access to cash | Medium/long-term savings, planned future expenses, funds you won’t touch soon |

So — Which One Should You Use,When?

It really depends on what you want from your money. Here are some guidelines to help decide:

✅ Use Demand Deposits If You Need:

- Quick access to funds for everyday expenses, groceries, bills or payrolls

- A buffer or emergency fund that you might need at a moment’s notice

- Liquidity and flexibility — no strings attached to withdrawing or spending

- A place to park cash short-term, without compromise on access

✅ Use Term Deposits If You Want:

- A safe, higher-yield savings option for money you don’t plan to touch soon

- Predictable, low-risk returns without dealing with stock markets or volatile investments

- To protect savings from impulsive use — by locking them until maturity

- To grow savings steadily for medium- or long-term goals (vacation fund, down payment, large purchase, etc.)

Common Mistakes & What to Watch Out For

- Using demand deposits as long-term savings — this means losing potential interest and exposes money to inflation erosion over time.

- Putting urgent funds in term deposits — if you need the money before maturity, you may suffer penalties or lose best rate benefits.

- Ignoring interest vs liquidity trade-off — sometimes people chase higher rates but forget they might need access to the funds earlier.

- Not checking bank policies — some demand-type savings or money-market accounts restrict certain withdrawals or have fees/limits. Always read the fine print.

A Smart Strategy: Use Both — the “Dual-Account” Approach

For many people (and businesses), a mix works best:

- Main “liquid” account (demand deposit): Keep enough to cover 3–6 months of expenses and cash-flow needs.

- “Locked-in” savings account (term deposit): Use for goals, surplus reserves, or money you won’t touch soon.

This way you get the best of both worlds: flexibility when you need it, and growth where you don’t. It’s a smart, risk-aware approach to managing money.

Final Thought

Understanding the difference between demand deposits and term deposits is a small but powerful step in managing your finances wisely. If you value ease-of-access, flexibility, and liquidity — demand deposits are your go-to. But if you’re looking to grow your savings with minimal fuss and don’t need the money immediately, term deposits offer a stronger return on idle cash.

In the end: use each type for what it’s best at. Keep your “ready cash” in demand-deposit accounts, and let your long-term savings sit tight and grow in term deposits. That balance can give you flexibility, security, and sensible returns — all at once.